Key takeaways:

- AI requires massive capital: Big tech alone is spending hundreds of billions annually; with global AI infrastructure needs projected to reach USD 6.7 trillion by 2030.

- Private funding can’t cover it all: Venture capital and corporate investment fall short, making government support and sovereign wealth funds crucial.

- Winner-takes-all dynamics are intensifying: Big tech incumbents dominate the market, with major implications for economic and strategic power.

- Governments must act strategically: National AI strategies, targeted investments, and global collaboration are essential to safeguard competitiveness and sustainable growth.

Big tech spent USD 155 billion on AI in FY 2025 and is set to invest hundreds of billions more. In total, 4 tech companies (Microsoft, Meta, Alphabet, and Amazon) will spend USD 369+ billion on capex (USD 400+ billion, by most accounts) in the coming year.

Source: Guardian News

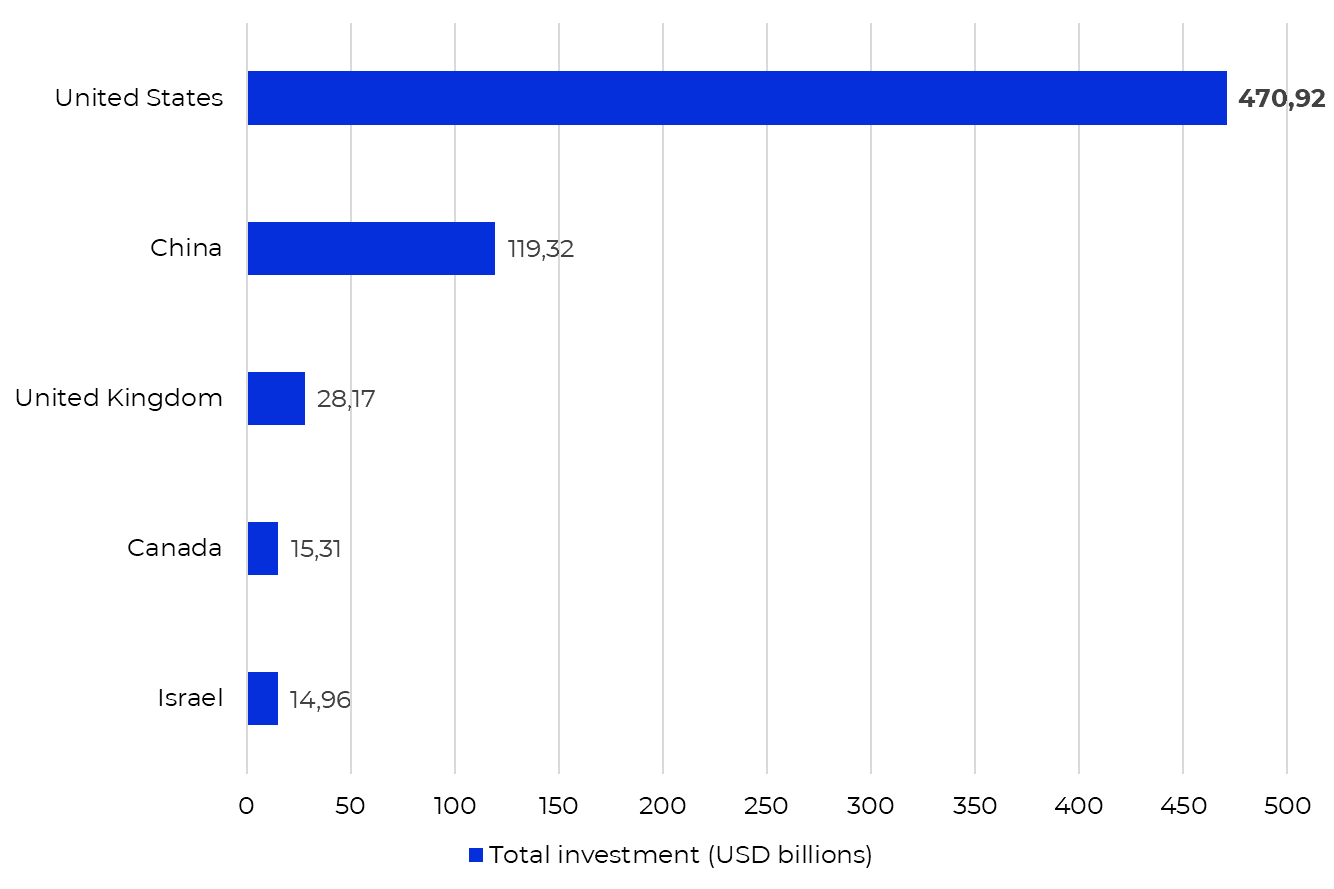

The number is huge if we compare it to private AI investment by country, aggregated over 2013-2024. Here’s the top 5:

Thus, tech giants in 12 months will spend nearly as much as business in the USA over the last 12 years. And the forecast values will only grow.

By the decade’s end, AI infrastructure is stated to require USD 6.7 trillion worldwide, mainly due to the escalating cost of compute. Remember to couple that with variable costs, e.g. OpenAI’s cash burn is estimated to soar from USD 8 billion in 2025 to 115 from USD 8 billion in 2025 to 115 billionthrough 2029.

The bottom line is, to sustain frontier AI efforts, huge financial backing is needed. Where do AI companies go?

AI funding sources: VC, big tech, and government investments

Global AI venture capital (VC) funding exceeded USD 100 billion in 2024 – a 62% YoY growth, still not enough to satisfy AI companies’ demand. For billions-scale infusions, they might turn to:

1. Private sector

Corporate AI investment reached USD 252.3 billion in 2024, hitting a record high with 26% growth.

2. Heavyweights

Big tech makes ‘equity investments’ in AI startups (e.g., Amazon's USD 4 billion investment in Anthropic or NVIDIA’s USD 100 billion investment in OpenAI). The problem is, a lot of that value is conditional, i.e. these are mostly cloud credits (or, as is the case with NVIDIA, GPUs), not cash. Additionally, this raises profitability concerns (Anthropic’s revenue tied to Amazon and Microsoft).

3. Governments

Governments provide AI leaders with grants, equity investments, subsidies and tax incentives, compute and infrastructure access, loans and accelerators.

Public sector AI funding initiatives

Source: SecondTalent

Though governments worldwide are increasingly channeling resources into AI, with China and the US at the forefront (USD 62 and 52 billion respectively), their commitments remain limited. Reasons may vary: shifting political priorities, risk considerations, skepticism or underestimation of AI’s future demand, or strategic reliance on the private sector.

4. Sovereign Wealth Funds (SWFs) (government-affiliated)

Since VC and private investments will not be sufficient, SWFs might become AI companies’ last resort. In 2024, SWFs’ total assets under management reached $12 trillion globally. GCC funds collectively manage USD 5 trillion (USD 7 trillion by 2027), among other large investors are China-, Norway- and Singapore-based SWFs.

Top 10 SWFs worldwide

Source: Global SWF

Direct AI allocations are still nascent though. Most exposure comes via equity holdings in major tech companies that also lead in AI.

Sovereign wealth funds AI investments

- NBIM’s (Norway) largest positions include Microsoft (USD ~43 billion), NVIDIA (USD ~35 billion), Amazon (USD ~23 billion), Meta (USD ~15 billion), and TSMC (USD 14 billion).

- Saudi PIF and Emirates’ Mubadala have made more targeted AI bets, e.g. in Mistral, Alat, and Databricks.

- QIA (Qatar) funded Builder.ai (USD 250 million), Databricks, and Ardian Semiconductor.

Source: FTI Consulting

That said, AI firms’ sources of financing are tight. Then the question is, whether there is enough capital in the world to sustain AI development.

If there is, those who deliver on promises could reap enormous rewards. But if capital does not prove sufficient, consequences might include systematic breakdowns, supply chain bottlenecks, regulatory backlash and, eventually, a surge of consolidations.

On top of that, many emerging AI companies build on existing models, ensuring incumbents’ recurring revenue, so, if funding dries up, integrators, not tech giants, are at risk.

AI industry outlook: winner-takes-all market risks

High costs, along with compute shortages, data monopolies, and capital intensity, drive strategic M&A (2025 total deal volume is expected to exceed that of the prior year by 33%), reducing diversity and shifting to state / incumbent control .

- Concentration of computing power and services

The US accounts for one third of the top 500 supercomputers and more than a half of overall computational performance.

Most of the leading semiconductor companies are from developed economies (NVIDIA’s 80-85% AI chip dominance).

The market of AI services providers is dominated by the US- and China-based companies (Amazon, Alphabet, IBM, Microsoft, OpenAI in the US and Baidu, Tencent in China).

Source: UNCTAD

- Vertical integration

OpenAI, Oracle, and SoftBank announced five new US AI data centers under Stargate, totaling nearly 7 gigawatts and $500 billion in investment, integrating hardware, models, and applications for national security.

Baidu, Alibaba, and Tencent formed alliances to build a domestic AI ecosystem amid U.S. export curbs.

- Startup acquisition and cloning

Workday announced a USD 1.1 billion acquisition of an AI startup Sana to sell agents alongside everyone from Salesforce and ServiceNow to SAP and Google.

- Closed systems block sharing

Big tech advocates for openness (e.g. OpenAI and Google challenging the UK government's AI copyright strategy), but as a rule copies without reciprocity, prioritizing profits over sharing.

Given that just 100 companies account for over 40% of global business R&D investment, large players locking up their technology can significantly hinder open innovation.

All together, these strains centralize resources and create a ‘winner-takes-all’ gap. As a result, AI is dominated by incumbents, raising concerns over economic dependence, limited innovation diversity, strategic vulnerabilities, and national competitiveness – forcing governments to take decisive steps.

Closing the AI funding gap: government playbook

While private enterprises, investors, and civil society play vital roles in responsible AI deployment, the greatest responsibility falls on governments due to the scale of investment needed and associated risks. That’s why, regardless of capital availability in the industry, governments should know how to act. Here are the steps we suggest they take:

- Determine AI direction and positioning: Decide whether to develop domestic capabilities, rely on international platforms, or combine both, guiding all policies and investments.

- Build a national AI strategy: Outline economic, technological, and geopolitical goals.

- Conduct supply-demand analysis across the AI value chain: Identify market needs, investment gaps, and sectors for targeted resource allocation.

- Align investment and funding mechanisms with strategic goals: Deploy capital through investments and partnerships that support prioritized areas, while balancing domestic innovation with dependence on global players.

- Advance international collaboration, workforce development, and regulation: Engage internationally on governance and ethics, while building workforce skills to sustain AI growth.

What approach do you think governments should take?

References

- Guardian News https://www.theguardian.com/technology/2025/aug/02/big-tech-ai-spending

- WSJ https://www.wsj.com/tech/ai/tech-ai-spending-company-valuations-7b92104b?mod=tech_trendingnow_article_pos2

- Stanford University https://hai.stanford.edu/assets/files/hai_ai_index_report_2025.pdf

- McKinsey https://www.mckinsey.com/industries/technology-media-and-telecommunications/our-insights/the-cost-of-compute-a-7-trillion-dollar-race-to-scale-data-centers

- Marketplace https://www.marketplace.org/story/2025/08/28/spending-on-ai-data-centers-could-run-to-the-trillions-of-dollars-by-the-end-of-the-decade

- CNBC https://www.cnbc.com/2025/09/06/openai-business-to-burn-115-billion-through-2029-the-information.html#:~:text=OpenAI%20has%20sharply%20raised%20its%20projected%20cash%20burn,popular%20ChatGPT%20chatbot%2C%20The%20Information%20reported%20on%20Friday.?msockid=0c43ad61af5b674d3eebbd1aae896619

- Fello AI https://felloai.com/2025/09/all-about-nvidias-100b-investment-in-openai-and-what-it-means-for-the-future-of-ai/

- Tech Monitor https://www.techmonitor.ai/digital-economy/ai-and-automation/global-ai-venture-capital-110bn-2024-driven-foundational-models

- Amazon https://www.aboutamazon.com/news/company-news/amazon-anthropic-ai-investment

- VentureBeat https://venturebeat.com/ai/anthropic-revenue-tied-to-two-customers-as-ai-pricing-war-threatens-margins

- SecondTalent https://www.secondtalent.com/resources/ai-startup-funding-investment/

- Deloitte https://www.deloitte.com/middle-east/en/about/press-room/gulf-sovereign-wealth-funds-lead-global-growth-as-assets-forecast-to-reach-usd18-tn-by-2030.html

- Diplo https://www.diplomacy.edu/blog/investment-diplomacy-in-action-with-gulf-sovereign-wealth-funds/

- Global SWF https://globalswf.com/ranking

- FTI Consulting https://www.fticonsulting.com/insights/articles/sovereign-wealth-funds-ai-investment-landscape

- Ropes & Gray https://www.ropesgray.com/en/insights/alerts/2025/08/artificial-intelligence-h1-2025-global-report

- Cryptopolitan https://www.cryptopolitan.com/nvidia-continues-to-dominate-the-ai-chip-market-despite-the-competition/?ysclid=mg4x06hi90270314446

- UNCTAD https://unctad.org/system/files/official-document/tir2025_en.pdf

- WIRED https://www.wired.com/story/openai-oracle-softbank-data-center-stargate-us/

- Reuters https://www.reuters.com/world/china/chinese-ai-firms-form-alliances-build-domestic-ecosystem-amid-us-curbs-2025-07-28/

- ListMyStartup https://www.listmystartup.app/article/workdays-11-billion-ai-acquisition-how-sana-deal-could-revolutionize-enterprise-learning

- Tech Monitor https://www.techmonitor.ai/digital-economy/ai-and-automation/openai-google-challenge-uk-ai-copyright-strategy?cf-view

- MIT NANDA https://mlq.ai/media/quarterly_decks/v0.1_State_of_AI_in_Business_2025_Report.pdf